题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

[主观题]

The date when the bill of lading is issued may be later than that stipulated in t

he credit.()

查看答案

如果结果不匹配,请 联系老师 获取答案

题目内容

(请给出正确答案)

如果结果不匹配,请 联系老师 获取答案

题目内容

(请给出正确答案)

如果结果不匹配,请 联系老师 获取答案

更多“The date when the bill of ladi…”相关的问题

更多“The date when the bill of ladi…”相关的问题

ACCOUNT NUMBER: 3752-A DATE: 5/8/2009

BUYER'S NAME: BRAD, FISHER

DATE PURCHASED: 4/15/2009

ADDRESS: 2515 SECOND AVE

CITY: PALM BAY STATE: FL ZIP; 32905

WORK PHONE: (321) 722-0795

HOME PHONE: (321) 956 - 2418

DRIVER LIC # : f - 260 - 065 - 3567 -1 DOB: 4/29/1969 SSN # :

212-99-3785

VEHICLE ID# : 1GDU789EOLKS64409 YEAR: 2003

MAKE: Dodge MODEL; Shadow

BODY STYLE. 4 Door COLOR: Aqua

PAYMENTS ARE DUE: 1

(1 = WEEKLY, 2 = BI - WEEKLY, 3 = MONTHLY, 4 = SEMI MONTHLY)

TOTAL PURCHASE PRICE: $6,122.21 TOTAL DOWN PAYMENT: $ 1,500.00 INITIAL BALANCE: $4,622.21 TOTAL PAID ON PURCHASE: $0.00

EACH PAYMENT-. $128.40 LAST PAYMENT DATE; 5/8/2009

NEXT PAYMENT DUE: 5/15/2009

TOTAL PAID ON MISC. CHARGES: $0.00

DECLINING BALANCE: $4,622.21

What is the birth date of Brad Fisher?

A.April 29th, 1969

B.April 15th, 1969

C.May 8th, 1969

D.May 15th, 2009

A.When the petty cash fund is initially establishe

B.On the date the petty cash funds are disburse

C.When the petty cash fund is replenishe

D.Only at the end of the accounting periods.

A.正确

B.错误

Witch measures non-controlling interest at fair value, based on share price.The market value of Wizard shares at the date of acquisition was $1.75.At 31 March 20X9 the retained earnings of Wizard were $750,000.

At what amount should the non- controlling interest appear in the consolidated statement of financial position of Witch at 31 March 20X9().

A、$195,000

B、$193,125

C、$135,000

D、$188,750

solstice.

In many of the Christian 【C14】______ , March25thisstillthe Feast of the Annunciation, when the Angel Gabriel 【C15】______ to Mazy that she【C16】______ the mother of Jesus.

【C17】______ impulse for the feast of Christmas may have came too 【C18】______ the establishment of the pagan feast of the "Unconquered Sun-God" by the Emperor Aurelian in 274 A.D. to be celebrated on December 25, the day of the winter solstice in Rome and throughout the empire. 【C19】______ , Christians could celebrate the feast of the "Sun of righteousness" (Malachi 4,2), Jesus Christ, who called himself" 【C20】______ of the world."

【C1】

A.religion

B.origin

C.region

D.oration

The following scenario relates to questions 11–15.

Alisa commenced trading on 1 January 2015. Her sales since commencement have been as follows:

The above figures are stated exclusive of value added tax (VAT). Alisa only supplies services, and these are all standard rated for VAT purposes. Alisa notified her liability to compulsorily register for VAT by the appropriate deadline.

For each of the eight months prior to the date on which she registered for VAT, Alisa paid £240 per month (inclusive of VAT) for website design services and £180 per month (exclusive of VAT) for advertising. Both of these supplies are standard rated for VAT purposes and relate to Alisa’s business activity after the date from when she registered for VAT.

After registering for VAT, Alisa purchased a motor car on 1 January 2016. The motor car is used 60% for business mileage. During the quarter ended 31 March 2016, Alisa spent £456 on repairs to the motor car and £624 on fuel for both her business and private mileage. The relevant quarterly scale charge is £294.

All of these figures are inclusive of VAT. All of Alisa’s customers are registered for VAT, so she appreciates that she has to issue VAT invoices when services are supplied.

From what date would Alisa have been required to be compulsorily registered for VAT and therefore have had to charge output VAT on her supplies of services?

A.30 September 2015

B.1 November 2015

C.1 October 2015

D.30 October 2015

What amount of pre-registration input VAT would Alisa have been able to recover in respect of inputs incurred prior to the date on which she registered for VAT?A.£468

B.£608

C.£536

D.£456

How and by when does Alisa have to pay any VAT liability for the quarter ended 31 March 2016?A.Using any payment method by 30 April 2016

B.Electronically by 7 May 2016

C.Electronically by 30 April 2016

D.Using any payment method by 7 May 2016

Which of the following items of information is Alisa NOT required to include on a valid VAT invoice?A.The customer’s VAT registration number

B.An invoice number

C.The customer’s address

D.A description of the services supplied

What is the maximum amount of input VAT which Alisa can reclaim in respect of her motor expenses for the quarter ended 31 March 2016?A.£108

B.£138

C.£180

D.£125

请帮忙给出每个问题的正确答案和分析,谢谢!

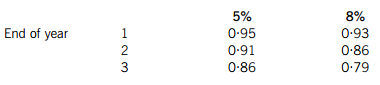

When preparing the draft financial statements for the year ended 30 September 2011, the directors are proposing to show the loan note within equity in the statement of financial position, as they believe all the loan note holders will choose the equity option when the loan note is due for redemption. They further intend to charge a finance cost of $500,000 ($10 million x 5%) in the income statement for each year up to the date of redemption.

The present value of $1 receivable at the end of each year, based on discount rates of 5% and 8%, can be taken as:

Required:

(a) (i) Explain why the nominal interest rate on the convertible loan notes is 5%, but for non-convertible loan notes it would be 8%. (2 marks)

(ii) Briefly comment on the impact of the directors’ proposed treatment of the loan notes on the financial statements and the acceptability of this treatment. (3 marks)

(b) Prepare extracts to show how the loan notes and the finance charge should be treated by Bertrand in its financial statements for the year ended 30 September 2011. (5 marks)

Observe that for the programmer,as for the chef,the urgency of the patron(顾客) may govern the scheduled completion of the task,but it cannot govern the actual completion.An omelette(煎鸡蛋),promised in two minutes,may appear to be progressing nicely.But when it has not set in two minutes,the customer has two choices—waits or eats it raw.Software customers have had (71) choices.

Now I do not think software (72) have less inherent courage and firmness than chefs,nor than other engineering managers.But false (73) to match the patron's desired date is much more common in our discipline than elsewhere in engineering.It is very (74) to make a vigorous,plausible,and job risking defense of an estimate that is derived by no quantitative method,supported by little data,and certified chiefly by the hunches of the managers.

Clearly two solutions are needed.We need to develop and publicize productivity figures,bug-incidence figures,estimating rules,and so on.The whole profession can only profit from (75) such data.Until estimating is on a sounder basis,individual managers will need to stiffen their backbones and defend their estimates with the assurance that their poor hunches are better than wish derived estimates.

(71)

A.no

B.the same

C.other

D.lots of